IMF published a report on stablecoins this week:

"Understanding Stablecoins"

PDF

Brief summary:

- Todor

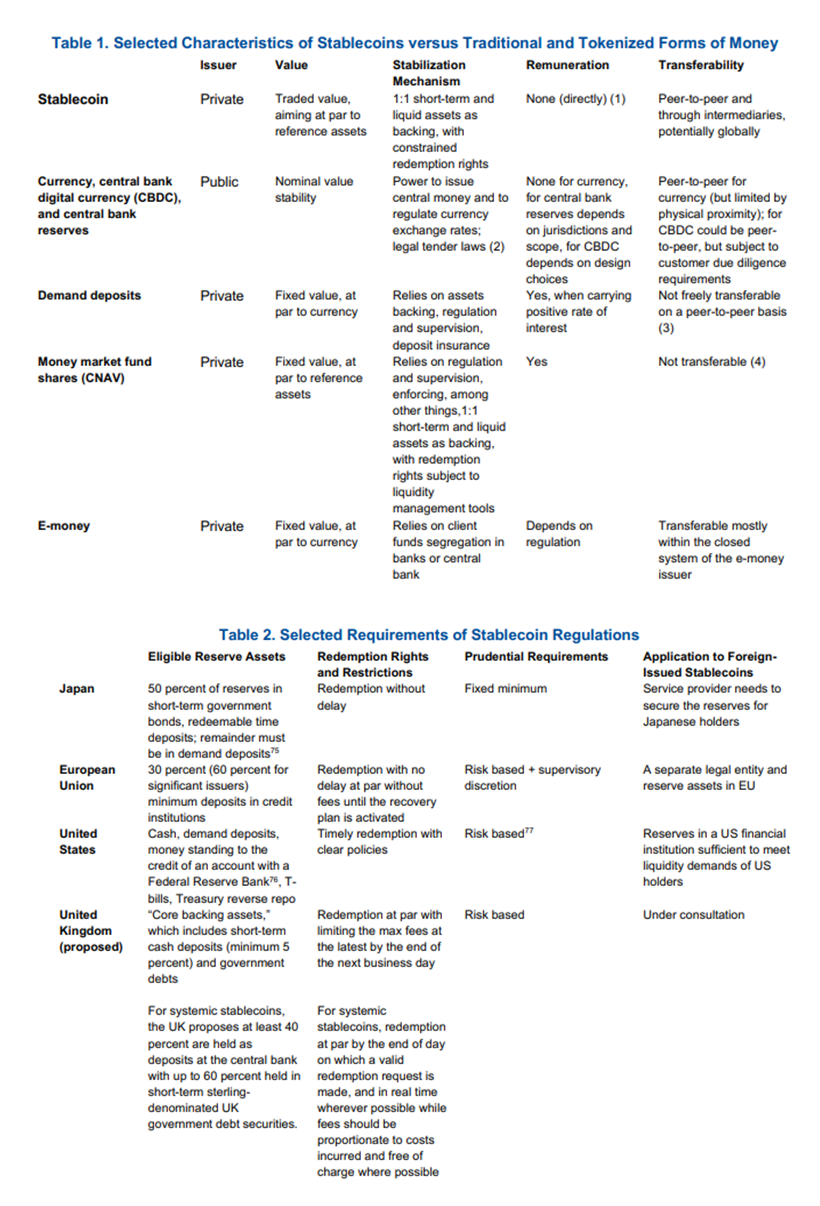

Excellent Post.A couple of tables within the document that complement the summary:

Great.

Thanks for adding additional colour Carlos.

CFA Society of the UK3rd floor, Boston House,63-64 New Broad Street, London EC2M 1JJ

About Us

Terms of Use

Cookie Policy

Privacy Policy